BACKGROUND

Donald Trump’s campaign promise not to tax tips or overtime pay is popular—despite helping relatively few workers—because it taps into the very real anger of low-income households struggling to make ends meet in a K-shaped economy. Their anger is justified. But the “solutions” included in Trump’s One Big Brutal Bill have left the tax code riddled with poorly designed Swiss-cheese tax cuts that sounded good on the campaign trail while doing nothing for most struggling American families.

When these tax cuts expire in a few years, Congress will be under tremendous pressure to extend them, creating a tax code permanently plagued with misguided tax incentives.

Instead, Congress can provide true, broad-based tax relief on the income that households need to meet their basic cost of living. Such a step would sharply reduce the pressure to maintain ad hoc carveouts while providing a real income boost to households as they strive to meet their basic needs.

Members of both parties have proposed legislation to cut taxes on low- and middle-income households, but they differ widely in how they’re drafted and who they impact—and several come with serious negative side effects!

THE WORKING AMERICANS TAX CUT ACT

Here are a few of the ways that the Working Americans Tax Cut Act, or WATCA for short (S. 4083/HR 7937) provides a boost to hardworking low-income households while avoiding the pitfalls of other proposals:

- WATCA provides targeted tax relief motivated by a simple, coherent, and intellectually defensible idea: the federal government shouldn’t tax the income necessary for basic survival. Estimates suggest that the basic cost of living for a single adult with no children is $46,000 a year. Low-income Americans are being squeezed by higher prices, stagnant wages, and reduced public services at the same time that they’re paying income taxes on the income they need to survive. No one would ever design such a system from scratch. WATCA gives these households a pocketbook win that they can bank immediately, building trust in political leaders while harder-to-implement solutions to the affordability crisis are moving forward.

- WATCA ensures that everyone gets treated fairly under the law and that no one is taxed into poverty. Instead of picking and choosing between different types of workers—waiters vs. mechanics, teachers vs. custodians—or filling the tax code with new loopholes and new ways to game the system, WATCA applies a universal standard to the income required to meet our basic human needs.

- WATCA is designed to complement EITC and CTC expansion without pitting the interests of the poorest Americans against those of other low-income workers who are struggling too. When policy decisions leave households in the bottom 40% behind, it breeds class resentment directed at the very poorest and plays directly into the hands of Trump and his billionaire friends.

WATCA’s sponsors have explicitly endorsed passing the bill as part of a larger package that includes an expansion of refundable tax credits. Workers who would not otherwise benefit from a package limited to EITC or CTC expansions would still see an increase in their take-home pay as a result of WATCA being included.

And workers who would see some benefit from EITC or CTC expansions would get a bigger boost from a package that included WATCA as well. In fact, even under current law, the addition of WATCA would make existing tax credits more generous—one reason why the bill would make 26 million children better off.

For example, a single worker with a child making $35,000 in 2025 would have owed federal income taxes of $1,138 before tax credits. Subtracting their $2,200 child tax credit and $2,462 earned income tax credit would have generated a refund of $3,524.

When combined with WATCA, however, their total refund would have grown from $3,524 to $4,162—an increase of $638. WATCA would have eliminated their federal income tax, letting them get back the entire $1,700 refundable portion of the child tax credit + $2,462 from the earned income tax credit.

Meanwhile, workers who have no income tax liability under existing law would benefit from the expansion of the refundable credits exactly as they would otherwise.

In short, every low-income household wins, with WATCA boosting the anti-poverty impact of existing refundable tax credits. While the cost to federal coffers is covered by millionaires!

- WATCA was intentionally drafted as an alternative maximum tax that phases out at higher income levels and NOT as an increase to the standard deduction.

That policy choice matters more than you might think because of how it impacts other areas of the tax code:

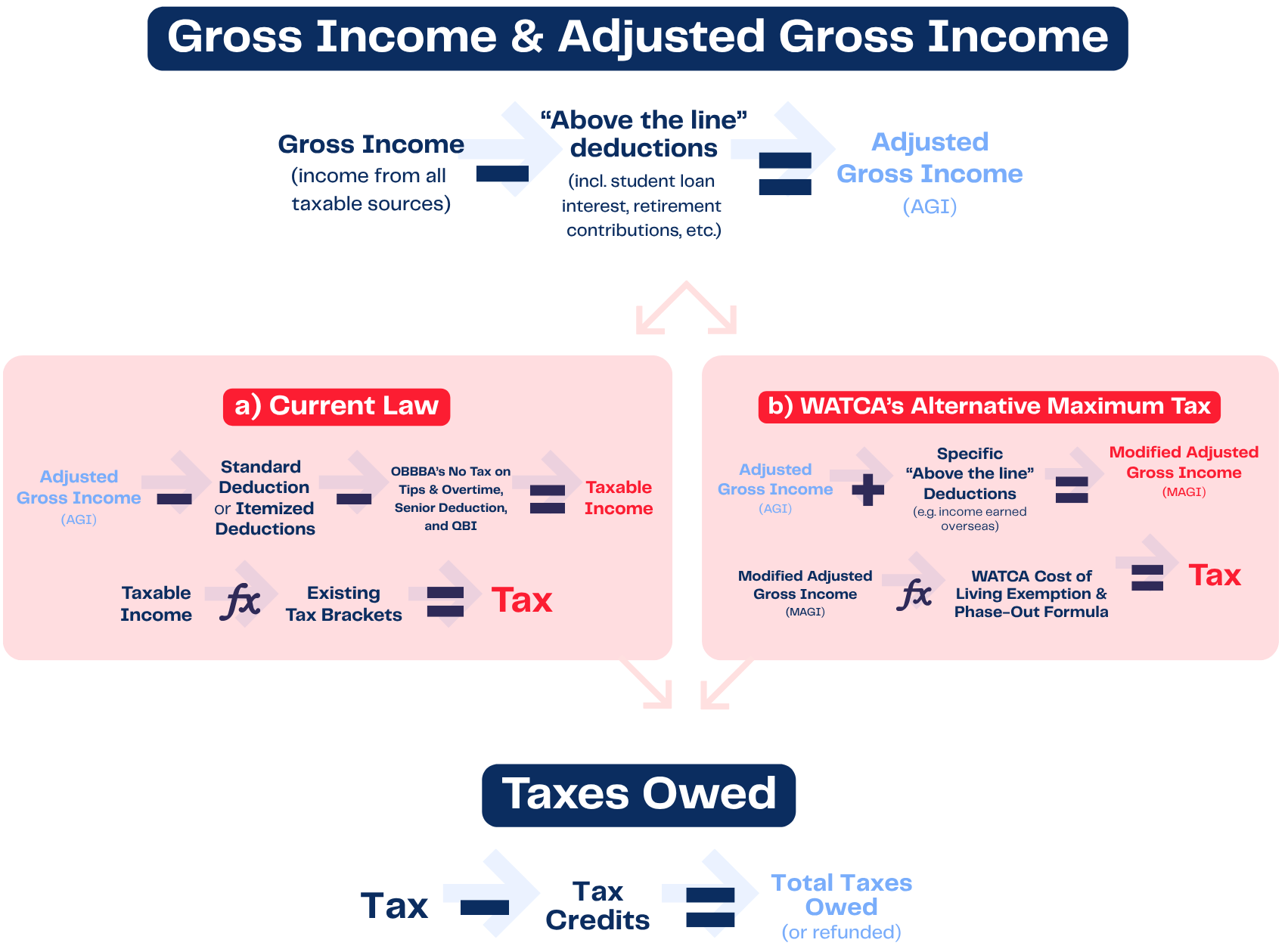

WATCA’s alternative maximum tax has an exemption of the first $46,000 (for individuals) and $92,000 (for married households filing jointly) that phases out for higher-income households.

That exemption generates tax cuts of about $3,300 (individual) and $6,600 (couples). Because of the phase-out, the tax cuts decline until they are zeroed out for incomes over $80,000 (individual) and $160,000 (couple).

Not only does this structure ensure that the cost-of-living tax cut is targeted to households making near the cost of living, the alternate maximum tax essentially wipes out the Swiss-cheese loopholes created by OBBBA, putting all workers on the same playing field—regardless of where their income comes from—and eliminates the potential for gaming the system.

WATCA’s alternative maximum tax also does NOT change how “taxable income” is calculated under the existing code, instead providing an alternative way of calculating tax. (The flowchart at the end of this explainer depicts how the current system and the WATCA alternative tax would work.)

This is important because several states have tied their state income taxes to federal taxable income. Changing the standard deduction risks negatively impacting state tax revenues in those states.

In contrast, proposals that rely on increasing the standard deduction fall short in several ways by:

- Creating a bigger deduction for higher-income taxfilers

- Allowing taxfilers to continue to claim the OBBBA provisions, ensuring that these loopholes and opportunities for gaming income continue

- Cutting state tax revenue in states that link their definition of taxable income to the federal definition